ALMM List-II Deadline Extended to 31 December 2026: What It Means for Solar Businesses India's

Read MoreThe Government of India has officially refused to grant any blanket extension to the June 1, 2026 deadline under the ALCM (ALMM List-II) policy. However, MNRE has clarified that projects where substantial investments or implementation steps were already completed before June 1, 2026 may be considered for case-to-case relief, subject to submission of supporting documents such as signed EPC agreements, connectivity approvals, approved electrical drawings, module delivery proof, and project execution evidence.

ALCM stands for Approved List of Cells and Manufacturers — effectively ALMM List-II. Where ALMM List-I regulates solar modules, ALCM extends that framework to solar cells. The ALCM Deadline in India is set for June 1, 2026, after which modules used in most solar projects must source their cells only from domestically approved manufacturers on this list.

MNRE announced this in December 2024. The goal is straightforward: push India’s solar supply chain upstream, from module assembly toward full cell manufacturing. It is the most ambitious step yet in that direction. And if recent moves are any indication, the government is not stopping at cells, in March 2026, MNRE expanded the ALMM framework further to include ingots and wafers under a new List-III, mandating their use from June 1, 2028. The upstream integration play is real, and it is moving fast.

India has built a formidable module manufacturing base. ALMM List-I module capacity has now surpassed 193 GW as of May 2026 — up sharply from the ~150 GW cited just months ago. But cell manufacturing has not kept pace.

ALMM List-II for solar cells has been revised seven times since first published on July 31, 2025, with the total enlisted capacity now reaching 30,508 MW across 13 manufacturers. That sounds like progress. It is — but it also exposes the structural gap: a 193 GW module industry being asked to source cells from a ~30 GW approved pool.

And nameplate capacity is not the same as deliverable capacity. Industry experts say effective stable TOPCon supply is only around 10–12 GW — a number that makes the 193 GW module base look even more exposed. Cell manufacturing involves chemical and thermal processes, requires specialized infrastructure like ETP and ZLD systems, and takes 15 to 24 months to set up. Several cell lines that were announced will not come online before 2027. Even larger players like Waaree Energies have struggled to meet deadlines and are still ramping up capacity.

Cell manufacturing costs around Rs 500 crore per GW to set up. Chinese cells remain cheaper. That price gap is the central anxiety for project developers.

The government also had to deal with another problem mid-stream: in October 2025, MNRE took serious note of government agencies issuing tenders with short bid submission timelines, clearly intended to circumvent the ALMM mandate on solar cells. It stated that any such tenders issued without complying with General Financial Rules and CVC regulations must, if necessary, be scrapped and new bids issued in full compliance. The message was blunt — the policy is not up for creative interpretation.

Developers want an extension, specifically until October 1, 2026. Several EPC firms and solar solution providers, including companies like Sun Photonics, are closely monitoring whether domestic TOPCon supply stabilizes before the June 2026 enforcement window.

Their argument is that current operational TOPCon capacity may lead to a supply–demand mismatch, project delays, and cost escalation once mandatory sourcing begins. TOPCon cell lines coming online now need at least six months to reach stable production. Forcing procurement from an unstable supply base creates execution risk, especially when developers have to give generation guarantees.

The expected shortage of DCR modules is likely to hamper the execution of nearly 20–25 GW of green open access projects over the next 2–3 years, and high prices of DCR modules will increase project tariffs by up to Rs 0.4–0.5 per unit.

Manufacturers are opposed. Their argument is equally blunt: sufficient TOPCon capacity exists, and every time the government delays a deadline, it signals that future delays are possible. That signal undermines the investment logic for building cell capacity in the first place and weakens confidence around ALMM List II solar cells compliance in India. ALMM itself was postponed twice, and manufacturers do not want a third precedent set.

Once a deadline is postponed, it tends to keep getting pushed further.

The irony is not lost on anyone: Renesys itself has now entered ALMM List-II, adding 452 MW of bifacial N-Type TOPCon solar cell capacity from its plant in Telangana. Hiranandani’s company now has skin in the game on both sides of the debate.

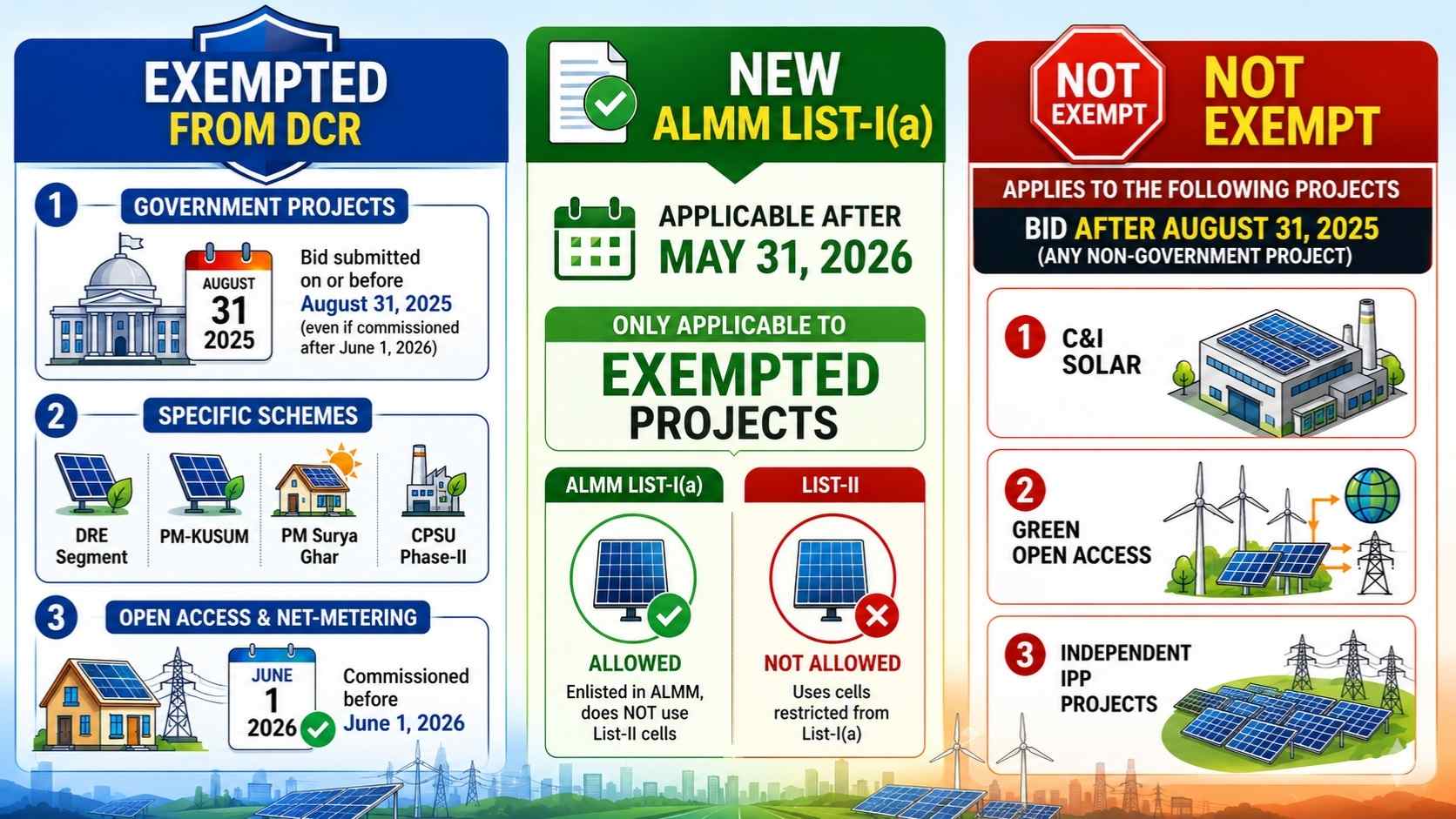

Government projects with bid submission dates on or before August 31, 2025 are exempt — even if commissioned after June 1, 2026. The DRE segment, PM-KUSUM, PM Surya Ghar, and CPSU Phase-II carry their own DCR provisions. Open access and net-metering projects commissioned before June 1, 2026 are also exempt.

After May 31, 2026, MNRE will maintain a new ALMM List-I(a) for solar PV modules that are enlisted in ALMM but do not use List-II cells — applicable only to exempted projects.

What is not exempt: any non-government project bid after August 2025. That is precisely where the growth pipeline sits: C&I solar, green open access, independent IPP projects.

As of today, MNRE has not moved. The June 1 date stands officially, and all signals from the ministry point toward holding the line. Several manufacturers have approached courts seeking relief, while others are urging the government to consider a more gradual implementation. The expectation in parts of the industry is that some form of flexibility will come — but that expectation is weakening with every passing week of ministerial silence.

At least for the next 18–24 months, capacity utilization will remain under pressure because domestic cell supply won’t be sufficient, say industry executives. Small players in the 500 MW to 1.5 GW range say even six months will not be enough. Some are asking for two years. That will not happen — the government has political capital invested in this policy, has already cracked down on circumvention attempts, and is now layering on wafer mandates for 2028. A full reversal is not on the table.

If anything changes, it will be narrow — a short transitional window with phased compliance thresholds. If nothing changes and the deadline holds, the worst-case scenario for small manufacturers is orders already freezing and factory shutdowns following shortly after.

The policy direction is right. India needs domestic cell capacity, and the government has already shown it is thinking two moves ahead with the wafer mandate for 2028. But the timeline for cells was set against supply realities that did not materialize. Thirteen days remain. Watch what MNRE does — or does not do — in that window. That decision will shape procurement strategies and project execution across India’s solar sector, including for EPC firms and solar solution providers like Sun Photonics.

Jatin Singh is a content developer at Sun Photonics Pvt. Ltd., specializing in creating impactful content for solar energy solutions. With a background in tech and health, he has previously worked in digital marketing and pharma. Passionate about sustainability, and currently exploring all things about solar!

Approval by an Expert:

“This content is reviewed and approved by Dr. Sujata Bhaker, who holds a Doctorate in Renewable Energy and brings over 10 years of industry expertise.”

ALMM List-II Deadline Extended to 31 December 2026: What It Means for Solar Businesses India's

Read More

ALMM Registration 2026: Who Can Apply, Complete Process, Documents & Profit/Loss Guide India's solar sector

Read More

For most Indian businesses, electricity is no longer a predictable monthly expense. It has become

Read More

Winters expose every weakness in a rooftop solar system — moisture, fog, temperature swings, metal

Read MoreThe ALCM deadline in India is June 1, 2026. After this date, most solar projects will be required to use solar cells sourced only from manufacturers approved under ALMM List II.

ALMM List II is the Approved List of Cells and Manufacturers introduced by MNRE to promote domestic solar cell manufacturing in India. It extends the ALMM framework beyond modules to solar cells.

As of now, MNRE has not officially extended the ALCM deadline. However, several developers and industry players are demanding a temporary extension due to limited domestic TOPCon cell capacity.

Green open access and net-metering projects commissioned before June 1, 2026 are exempt. Projects commissioned after the deadline may need to comply with ALMM List II solar cell requirements.

The ALCM mandate could increase procurement costs due to limited domestic cell availability and higher DCR module prices, potentially increasing solar tariffs by Rs 0.4–0.5 per unit.